VAT simplification also applies to four-party supply chains

VAT simplification also applies to four-party supply chains

International trade flows often involve multiple parties and EU Member States. The VAT rules applicable to such supply chains are complex, particularly when more than three parties are involved. Recently, the General Court of the European Union provided clarification on the application of simplified triangulation for VAT in a supply chain involving four parties established in three different EU Member States.

The General Court of the European Union ruled that simplified triangulation should be interpreted broadly. It is not required that the goods physically arrive at the third party: it is sufficient that this party obtains the power to dispose of the goods as owner, even if the goods are immediately delivered to a fourth party. Whether the intermediary is aware of the delivery to a fourth party is not relevant. The purpose of the scheme is to prevent a VAT registration obligation for the intermediary operator in the Member State of arrival. In cases of VAT fraud, the EU Member State may still refuse the application of the scheme and VAT may be levied in the country of where the intermediary operator is registered for VAT (Slovenia in this case). This is only possible if the intermediary operator knew or should have known about the VAT fraud.

The judgment emphasizes that for the application of the scheme, it does not matter whether the goods physically arrive at party C, as long as this party is VAT-registered in the country of arrival. This provides clarity and can reduce administrative burdens for entrepreneurs.

Facts of the case

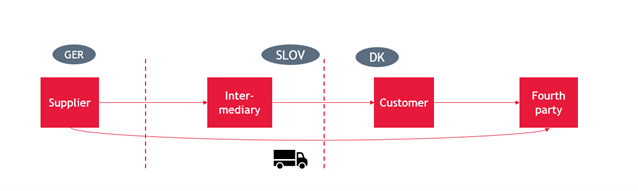

In this case, a Slovenian company purchased goods from a German supplier and sold them directly to Danish customers. The goods were transported directly from Germany to Denmark and ultimately ended up with a fourth party in Denmark. The Slovenian company, acting as the intermediary operator in the chain, applied simplified triangulation, which, according to the company, meant that no VAT was due in Denmark. However, the Slovenian tax authorities disagreed, arguing that the goods did not end up with the third party (the Danish customers of the Slovenian company), but with a fourth party. The question is whether simplified triangulation also applies if the goods do not physically arrive at the third party, but at a subsequent party in the chain. Importantly, in this case, that subsequent party is also established in the EU Member State of the third party: Denmark. The supply chain can schematically be represented as follows.The General Court of the European Union ruled that simplified triangulation should be interpreted broadly. It is not required that the goods physically arrive at the third party: it is sufficient that this party obtains the power to dispose of the goods as owner, even if the goods are immediately delivered to a fourth party. Whether the intermediary is aware of the delivery to a fourth party is not relevant. The purpose of the scheme is to prevent a VAT registration obligation for the intermediary operator in the Member State of arrival. In cases of VAT fraud, the EU Member State may still refuse the application of the scheme and VAT may be levied in the country of where the intermediary operator is registered for VAT (Slovenia in this case). This is only possible if the intermediary operator knew or should have known about the VAT fraud.

The Situation in the Netherlands

For Dutch practice, this judgment is relevant because it confirms that simplified triangulation can also be applied in longer supply chains, as long as the parties involved are registered for VAT in the relevant EU Member States. In the Netherlands, according to the policy decree on the ‘quick fixes,’ simplified triangulation applies if the Netherlands is the country of party A or B, or if parties C and D are established in the Netherlands and the Netherlands is the country of arrival. The State Secretary requires that party C must be established in the Netherlands if the Netherlands is the country of arrival. This means that from a Dutch perspective, simplified triangulation cannot be applied if the Netherlands is the country of arrival and the third party in the chain is not established in the Netherlands. This establishment requirement does not follow from the European VAT Directive and appears to conflict with the purpose of the scheme, as also indicated by the European Commission. In our opinion, entrepreneurs should be able to disregard this requirement by invoking the VAT Directive.The judgment emphasizes that for the application of the scheme, it does not matter whether the goods physically arrive at party C, as long as this party is VAT-registered in the country of arrival. This provides clarity and can reduce administrative burdens for entrepreneurs.